Overview of Yamal LNG shipment activity in 2025

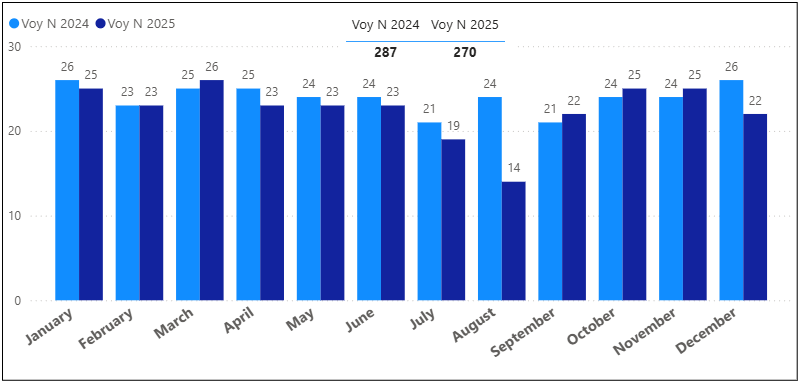

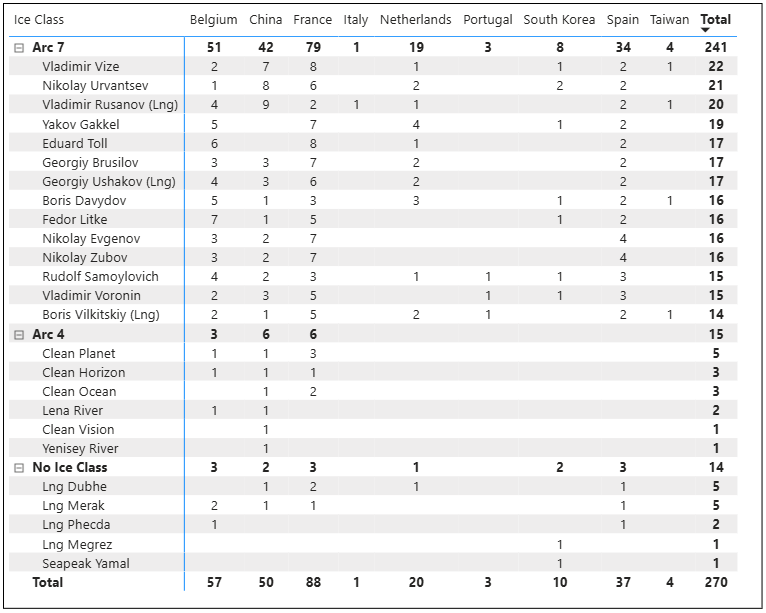

According to our calculations, the Yamal LNG project completed 270 shipments from the port of Sabetta in 2025. For comparison, 2024 was a record year with 287 shipments.

Graph 1. Monthly number of voyages from Sabetta in 2025 and 2024

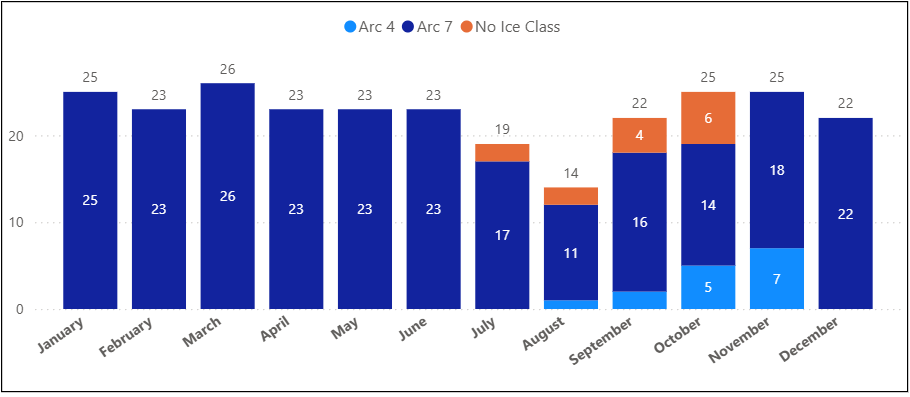

Throughout the year, the core export volume was delivered by 14 Arc7 ice‑class LNG carriers, which operated continuously and performed 241 voyages. By contrast, Arc4 vessels and non–ice‑class vessels worked only seasonally. From January to June, they did not load directly in Sabetta and instead received LNG via transshipment near Kildin Island before proceeding to ports in Europe and Asia. In the second half of the year, from August to November, 6 Arc4 vessels completed 15 shipments from Sabetta, while 5 non–ice‑class vessels operated from August to October and performed 14 shipments.

Graph 2. Monthly distribution of voyages by ice‑class category

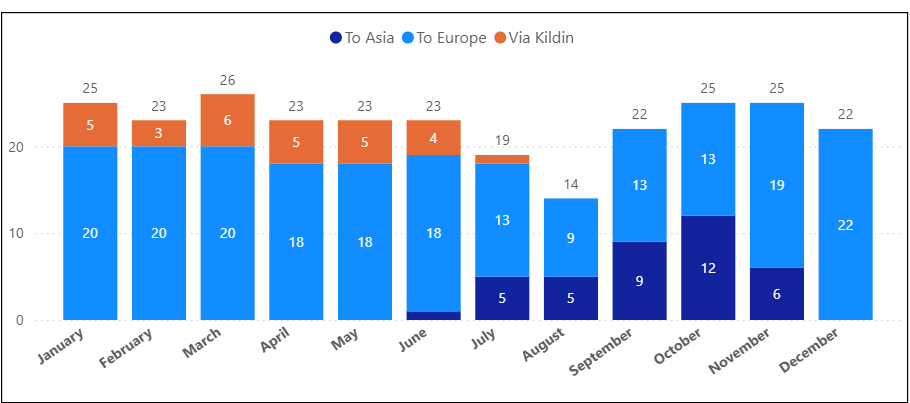

We also classified the voyages by destination. The chart below shows the monthly number of departures from Sabetta grouped into three categories: shipments to Europe, shipments to Asia, and shipments involving transshipment near Kildin Island. In cases where cargo was transshipped onto another vessel at Kildin, 26 out of 29 such voyages proceeded to Asia, while 3 went to Europe.

Graph 3. Monthly distribution of voyages by destination

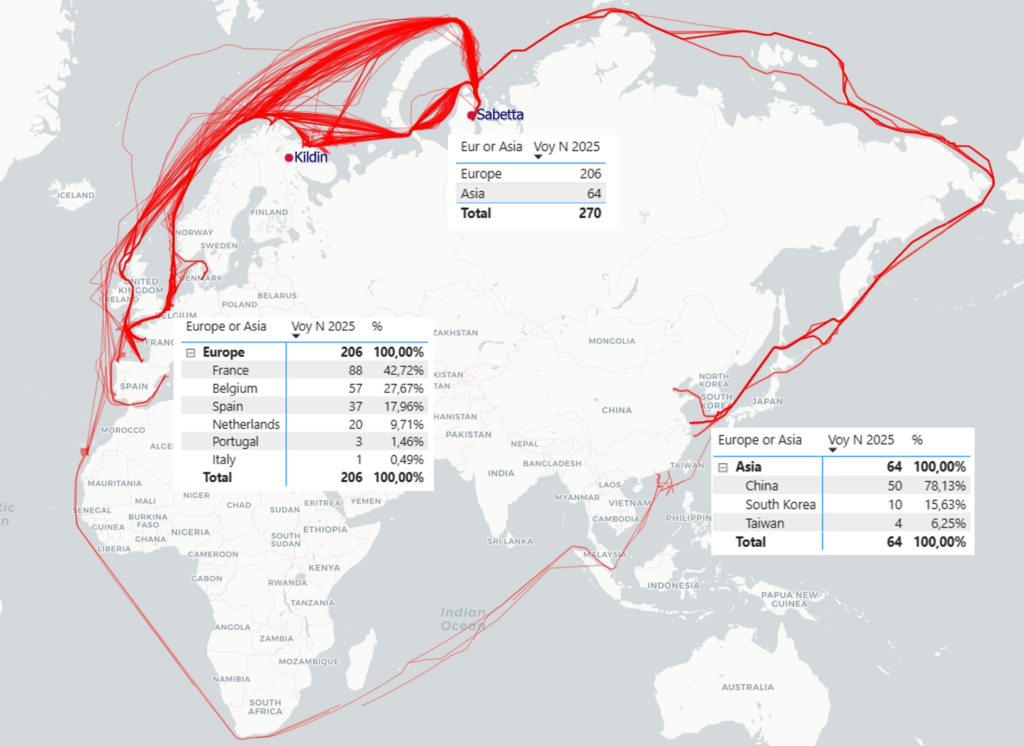

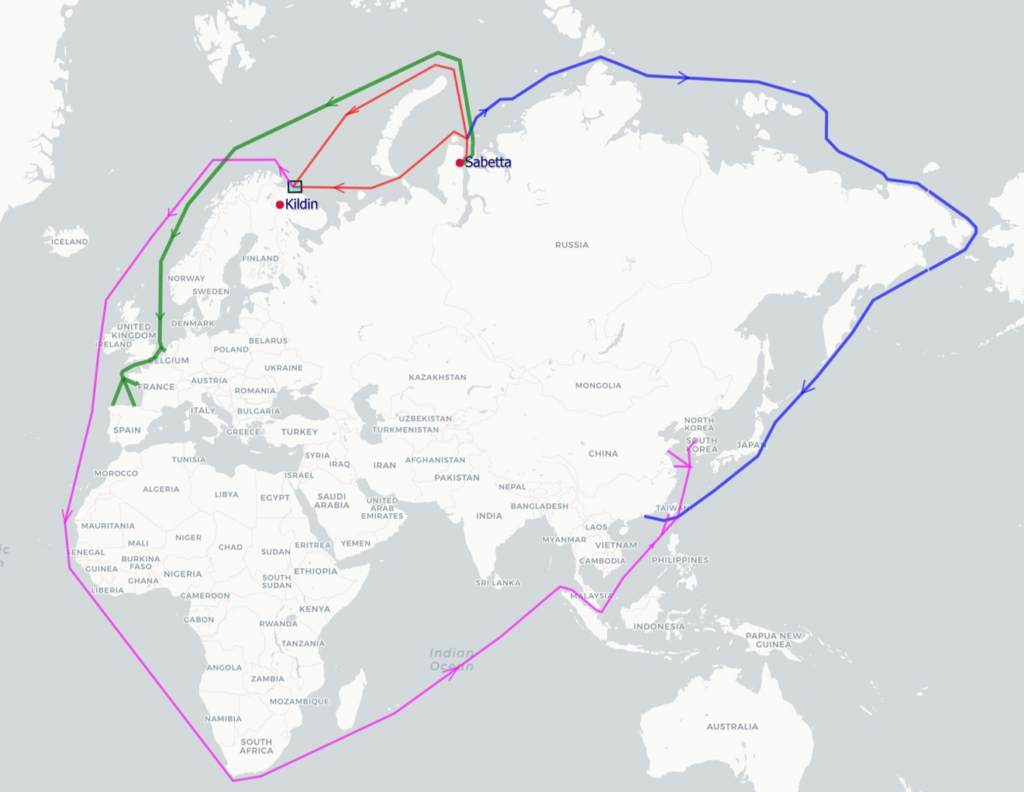

Map 1. Selected vessel tracks of the Yamal LNG fleet in 2025.

Based on the table below, the largest number of voyages in 2025 were directed to France, Belgium, and China, which together accounted for the majority of all departures from Sabetta. France received 88 voyages, making it the single most frequent destination. Belgium followed with 57 voyages, and China received 50 voyages. These three countries together absorbed more than two‑thirds of the total annual shipments.

Other destinations included Spain (37 voyages), the Netherlands (20 voyages), and Italy (1 voyage), while South Korea, Portugal, and Taiwan received much smaller numbers. Detailed vessel‑by‑vessel data for each destination is presented in the table below.

Table 1. All voyages from the port of Sabetta, including 29 voyages to Kildin Island for transshipment. The table indicates the destination country after the cargo is transshipped at Kildin.

Routing practices and transport patterns in 2025

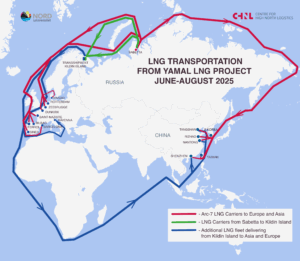

In 2025, LNG from Sabetta was exported through several routing options. The main route remained direct deliveries to European ports, which accounted for 203 voyages. Average sailing time from Sabetta to Europe was 8.83 days, and the average interval between consecutive voyages of the same vessel was about 22 days. Some voyages in early 2025 may have involved transshipment in Europe, but after 27 March 2025 such operations were no longer permitted.

A small number of shipments to Europe were routed through Kildin Island, but there were only 3 voyages, making this pattern statistically insignificant. Another important routing option was the southern route to Asia via Kildin, used 26 times, all in the first half of the year. The full delivery time from Sabetta via Kildin to Asia averaged around 50 days, while a complete round trip from Kildin to Asia and back required roughly 90 days.

Scheme 1. Main LNG transportation routes in 2025.

Direct southbound voyages from Sabetta to Asia accounted for 10 shipments, mainly carried out by Arc4 and non–ice‑class vessels after they completed the seasonal loading in Sabetta. In addition, 28 voyages to Asia were made via the Northern Sea Route (NSR) between June and November, all by Arc7 vessels. Based on actual voyage sequences, a full NSR round trip during the navigation season can be estimated at approximately 40 days.

In total, 206 voyages (76%) were directed to Europe, while 64 voyages (24%) went to Asia. This structure will inevitably change due to the upcoming EU regulatory measures, which will fully close the European market for Russian LNG from 1 January 2027.

Estimated transport capability after the shift to Asia

To understand the impact of redirecting all Yamal LNG shipments to Asia, we performed an approximate calculation of the fleet’s transport capability under post‑2027 conditions. The calculation uses the operational fleet: 14 Arc7, 6 Arc4, and 5 non–ice‑class vessels. The goal was to obtain an approximate estimate of the scale of change rather than a detailed schedule. The model does not account for maintenance, weather delays, port congestion, or precise synchronization of transshipment cycles.

Our estimate suggests that, if all flows are redirected to Asia, the fleet will be able to complete approximately 120 – 130 voyages per year. This is more than 2× lower than the export volumes of 2024–2025. The reduction is explained by longer distances to Asia, the limited NSR navigation window, dependency of Arc4 and non‑ice‑class vessels on transshipment operations, and the loss of short European routes that previously ensured high turnover. Even under favorable assumptions, the transportation capacity of the fleet decreases by more than half. In practice, actual capacity is likely to be even lower. Therefore, the logistics scheme will require adjustments, including possible expansion of ice‑class tonnage, increased transshipment capacity, or the introduction of alternative routing and storage solutions.

Export dynamics in the first quarter of 2026

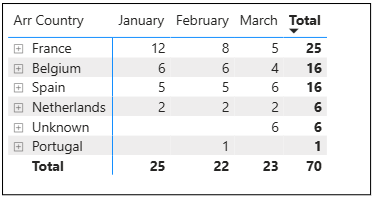

To illustrate the current operational situation ahead of upcoming restrictions, we analysed Yamal LNG shipments for the first 3 months of 2026. As of 31 March 2026, a total of 70 departures from Sabetta were recorded, all carried out by Arc7 vessels.

Table 2. LNG deliveries by arrival country in January–March 2026

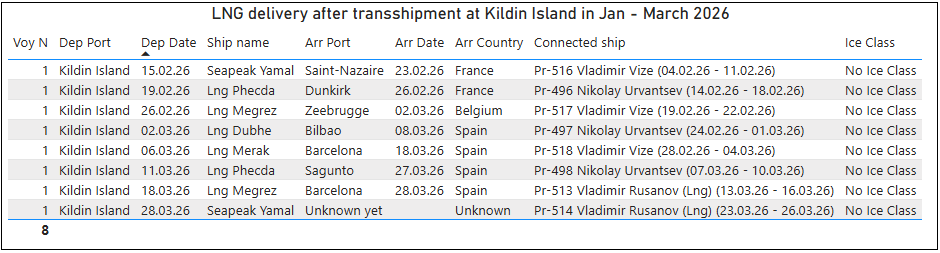

Of these, 8 voyages were directed first to the Kildin transshipment area. For 7 voyages, the final destination in Europe is confirmed, while the remaining voyage is still en route but its AIS track indicates a European destination. The other 62 voyages were delivered directly from Sabetta to European ports. Thus, 100% of all shipments in January, February, and March 2026 were directed to Europe.

Table 3. LNG deliveries after transshipment at Kildin Island in January–March 2026

For comparison, in the first quarter of 2025 there were 74 voyages, of which 14 went through Kildin and were subsequently delivered to Asia, while 60 went directly to Europe. This means that Europe received 60 voyages in Q1 2025 and 70 voyages in Q1 2026.

Conclusion

The data shows that Europe remains the dominant export destination for Yamal LNG in early 2026. However, due to forthcoming EU restrictions, a complete reorientation of exports to Asia is unavoidable. Under such conditions, the productive capability of the existing fleet will fall significantly. Without additional ice‑class vessels, expanded transshipment capacity, or redesigned logistics schemes, the current fleet will not be able to support export volumes comparable to previous years.